Added: Oct 30, 2025

Last edited: Oct 30, 2025

Polyethylene (PE) is one of the most widely used and versatile plastics worldwide. Known for its cost-effectiveness, flexibility, and durability, it plays a critical role in multiple industries such as packaging, construction, automotive, and consumer goods. According to Fortune Business Insights, the global polyethylene market continues to expand due to growing demand across industrial and consumer sectors.

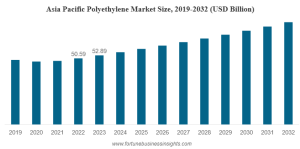

According to Fortune Business Insights, The global polyethylene market was valued at USD 110.23 billion in 2023 and is anticipated to increase from USD 114.89 billion in 2024 to USD 158.49 billion by 2032, reflecting a CAGR of 4.1% during the forecast period. Asia Pacific emerged as the leading region, accounting for 47.98% of the global market share in 2022. In addition, the U.S. polyethylene market is expected to experience substantial growth, reaching approximately USD 22.31 billion by 2032, fueled by rising demand from the packaging sector, ongoing technological advancements, growing sustainability initiatives, and favorable economic developments.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/polyethylene-pe-market-101584

LIST OF KEY COMPANIES PROFILED:

LyondellBasell Industries N.V. (Netherlands)

ExxonMobil Chemical (U.S.)

SABIC (Saudi Arabia)

Reliance Industries Limited (India)

INEOS (U.K.)

China National Petroleum Corporation (China)

China Petroleum & Chemical Corporation (China)

Ducor Petrochemicals (Netherlands)

Formosa Plastic Group (Taiwan)

Braskem (Brazil)

Market Size & Growth Forecast

The global polyethylene market was valued at USD 110.23 billion in 2023 and is projected to reach USD 158.49 billion by 2032, exhibiting a CAGR of around 4.1% during the forecast period (2024–2032).

Earlier estimates showed growth from USD 106.14 billion in 2022 to USD 140.21 billion by 2029, maintaining the same CAGR of 4.1%.

This consistent growth pattern indicates that the polyethylene market is stable and mature, driven by steady demand rather than rapid expansion.

Key Growth Drivers

Strong Demand from Packaging Sector

Packaging remains the largest application segment for polyethylene. Its light weight, chemical resistance, and flexibility make it ideal for films, containers, pouches, and wraps. The increasing use of flexible packaging in food, beverages, and consumer goods continues to boost PE demand.

Expanding End-Use Industries

Expanding End-Use Industries

The automotive, electrical & electronics, construction, and agriculture sectors are contributing significantly to polyethylene consumption. Its use in pipes, insulation, tanks, and protective films is increasing as infrastructure projects grow globally.

Manufacturing Expansion

Key producers are investing in new production facilities and advanced polymer technologies, increasing global supply and introducing high-performance PE grades to meet rising demand.

Segmentation Analysis

By Type

High-Density Polyethylene (HDPE)/Medium-Density Polyethylene (MDPE) – Dominates the market due to high tensile strength, chemical resistance, and usage in pipes, containers, and bottle caps.

Low-Density Polyethylene (LDPE) – Used in film applications, coatings, and packaging.

Linear Low-Density Polyethylene (LLDPE) – Offers flexibility and toughness, commonly used in stretch wraps and industrial films.

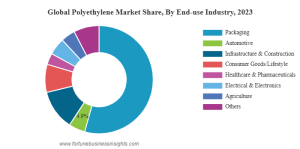

By End-Use Industry

Packaging – Holds the largest market share, driven by flexible packaging for food and e-commerce.

Infrastructure & Construction – Includes HDPE pipes, geomembranes, and insulation materials.

Healthcare & Pharmaceuticals – Used for medical packaging and devices.

Regional Insights

Asia-Pacific – The largest and fastest-growing market due to rapid industrialization, urbanization, and increasing infrastructure projects in China, India, and Southeast Asia.

North America – Growth driven by advanced packaging and construction applications, supported by low-cost shale gas feedstock.

Europe – Focused on sustainability, recycling, and regulatory compliance in plastic usage.

Middle East & Africa – Emerging as a key production hub due to abundant raw materials and growing downstream demand.

Latin America – Steady growth supported by food packaging and consumer goods demand.

Market Challenges

Feedstock Price Volatility

Polyethylene production depends on ethylene derived from petroleum or natural gas. Fluctuations in crude oil prices directly impact production costs and profit margins.

Environmental & Regulatory Pressure

Increasing bans on single-use plastics and mandates for recyclable materials challenge producers to innovate in sustainable and bio-based polyethylene alternatives.

Competition from Substitutes

Materials like polypropylene (PP), polyethylene terephthalate (PET), and biodegradable plastics are gaining traction as alternatives to conventional PE.

Market Saturation in Mature Regions

In developed economies, where packaging markets are already highly penetrated, growth is slower compared to emerging regions.

Strategic Insights

Companies should focus on developing sustainable and recyclable polyethylene grades to align with global circular economy goals.

Regional integration and cost optimization will be key for maintaining competitiveness as global supply expands.

Investment in advanced recycling technologies and eco-friendly production methods will help companies meet regulatory demands and enhance brand value.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/polyethylene-pe-market-101584

Future Trends

Increasing adoption of bio-based and recycled polyethylene to meet sustainability targets.

Greater focus on chemical recycling for circular polymer supply chains.

Continued expansion in Asia-Pacific and the Middle East driven by infrastructure development and feedstock availability.

The polyethylene market is projected to maintain steady growth over the next decade, reaching approximately USD 158.49 billion by 2032. Packaging remains the dominant application, while innovation in sustainable and advanced polymer technologies will shape the industry’s future.

Although the market faces challenges related to cost fluctuations and regulatory pressures, opportunities in recycling, lightweight materials, and emerging economies provide significant potential for long-term expansion.

KEY INDUSTRY DEVELOPMENTS:

November 2023: NOVA Chemicals Corporation and Amcor announced the signing of a Memorandum of Understanding (MoU) for mechanically recycled polyethylene. As per the agreement, NOVA Chemicals Corporation, the leading producer of polyethylene, would supply mechanically recycled polyethylene to Amcor, a prominent global packaging solutions manufacturer.